How to Value a SaaS Company: The Complete 2026 Guide

Revenue multiples, DCF, SDE, Rule of 40 - every SaaS valuation method explained with 2026 benchmarks, comparison tables, and common mistakes that kill deals.

I have sat across the table from founders who thought their SaaS company was worth $50M and watched a buyer’s advisor calmly explain why the number was $12M. I have also seen bootstrapped founders with $3M ARR leave $10M or more on the table because they did not understand what drives multiples.

SaaS valuations are not guesswork. They are not “whatever the market will bear.” There are specific methods, specific metrics, and specific mistakes that separate a company valued at 4x ARR from one valued at 12x ARR. This guide covers all of them.

Whether you are raising capital, planning an exit, evaluating an acquisition, or just trying to understand what your business is worth today, this is the framework you need. We will cover every major valuation method, the 2026 benchmarks you should be measuring against, and the mistakes that kill deals before they close.

Full disclosure: PipelineRoad operates both a B2B SaaS marketing agency and an AI capital raising platform. We work with fund managers and SaaS founders daily on both sides of the valuation equation. This guide reflects what we actually see in the market, not textbook theory.

Why SaaS Valuations Are Different from Every Other Business

A SaaS company is not a restaurant. It is not a law firm. It is not a manufacturing business. The valuation frameworks that work for those businesses will produce wildly incorrect results when applied to recurring revenue software.

Here is why:

Recurring revenue changes everything. A traditional business earns revenue when a customer buys something. When the customer stops buying, the revenue stops. A SaaS business earns revenue continuously through subscriptions. This makes future cash flows significantly more predictable, and predictability commands a premium.

Gross margins are structurally higher. Most SaaS companies operate at 70-85% gross margins. Compare that to manufacturing (20-35%), retail (25-50%), or professional services (30-50%). Higher margins mean more of each revenue dollar flows to the bottom line, which means acquirers and investors will pay more per dollar of revenue.

The asset is the code, not inventory. Software can be sold to one customer or one million customers with marginal cost approaching zero. This scalability is the fundamental reason SaaS multiples exceed those of nearly every other business type.

Customer lifetime value compounds. With strong retention, each cohort of customers generates revenue for years. A SaaS company with 95% annual retention keeps its customers for an average of 20 years. That is not a revenue stream - it is an annuity.

Network effects and switching costs create moats. Once a company’s workflow depends on your software, switching costs create a natural barrier. This defensibility is reflected in higher multiples.

The implication: you cannot value a SaaS company using methods designed for asset-heavy businesses. You need SaaS-specific approaches.

The Five Core SaaS Valuation Methods

There is no single “correct” way to value a SaaS company. Different methods work better at different stages, and sophisticated buyers and investors use multiple methods to triangulate a range. Here are the five you need to understand.

Method 1: Revenue Multiple (ARR Multiple)

This is the most common method for SaaS companies, and the one you will hear referenced most often in board meetings, pitch decks, and M&A discussions.

How it works: Take the company’s Annual Recurring Revenue (ARR) and multiply it by a factor. That factor - the multiple - is determined by growth rate, retention, margins, market, and dozens of other variables.

Formula: Valuation = ARR x Revenue Multiple

Example: A company with $5M ARR at a 7x multiple is valued at $35M.

When to use it: Post-product-market-fit companies with at least $1M ARR. This is the default method for SaaS companies between $1M and $100M ARR, and it is how most venture-backed SaaS companies are valued during fundraising.

2026 Revenue Multiple Benchmarks:

| Company Profile | Typical Multiple Range | Key Driver |

|---|---|---|

| Pre-revenue / pre-PMF | 1-3x (often on projected ARR) | Team, TAM, traction signals |

| $1-5M ARR, 20-40% growth | 3-6x | Retention, margin profile |

| $5-20M ARR, 30-50% growth | 5-10x | Rule of 40 score, NRR |

| $20-50M ARR, 40%+ growth | 8-15x | Market position, efficiency |

| $50M+ ARR, 30%+ growth | 10-20x+ | Category leadership, IPO potential |

What moves the multiple up:

- Net revenue retention above 120%

- Revenue growth above 40% YoY

- Gross margins above 80%

- Low customer concentration (no single customer above 10% of ARR)

- Strong unit economics (LTV:CAC above 3:1)

What moves the multiple down:

- High logo churn (above 10% annually)

- Customer concentration risk

- Founder dependency

- Declining growth rates

- Below-market gross margins

The biggest mistake with revenue multiples: Using public company multiples as your benchmark. Public SaaS companies trade at a premium because of liquidity - you can sell your shares tomorrow. Private SaaS companies apply a “liquidity discount” of 20-40%. A public company at 10x ARR does not mean your private company with similar metrics is worth 10x. It is probably worth 6-8x.

Method 2: SDE (Seller’s Discretionary Earnings)

SDE is the preferred method for smaller, owner-operated SaaS companies - typically those under $5M ARR where the founder is deeply involved in operations.

How it works: Start with net income, then add back the owner’s salary, benefits, one-time expenses, and discretionary spending. The result is the true cash flow the business generates for an owner-operator.

Formula: SDE = Net Income + Owner’s Compensation + One-Time Expenses + Non-Cash Expenses + Discretionary Expenses

Valuation = SDE x Multiple

SDE Multiple Ranges for SaaS (2026):

| ARR Range | SDE Multiple | Notes |

|---|---|---|

| Under $500K | 2-3x | High risk, founder-dependent |

| $500K-$2M | 3-4x | Emerging product-market fit |

| $2M-$5M | 4-5x | Established, potential to scale |

When to use it: Bootstrapped SaaS companies with under $5M ARR, especially those sold through online brokerages (Quiet Light, FE International, MicroAcquire/Acquire.com). Buyers at this level are often individual operators or small PE firms who care about cash flow, not growth-at-all-costs narratives.

What gets added back to SDE:

- Owner’s salary (often the biggest add-back)

- Owner’s health insurance, retirement contributions

- One-time development costs (rebuilt the app, migrated infrastructure)

- Personal expenses run through the business

- Non-recurring legal or consulting fees

What does NOT get added back:

- Expenses that a new owner would need to replicate

- Employee salaries (unless the owner is doing work an employee should do)

- Marketing spend that drives growth

The biggest mistake with SDE: Aggressive add-backs that no buyer will accept. I have seen sellers add back $200K in “marketing experiments” that were actually the core acquisition channel. Buyers are not stupid. They will scrutinize every add-back, and aggressive ones kill trust faster than a low revenue number.

Method 3: EBITDA Multiple

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is the standard for larger, more mature SaaS companies - typically those above $5M ARR with a professional management team.

How it works: Calculate EBITDA, then apply a multiple. Unlike SDE, EBITDA does not add back owner compensation because the assumption is that a professional manager is (or will be) running the company.

Formula: EBITDA = Revenue - COGS - Operating Expenses (before interest, taxes, depreciation, amortization)

Valuation = EBITDA x Multiple

EBITDA Multiple Ranges for SaaS (2026):

| Company Size | EBITDA Multiple | Context |

|---|---|---|

| $5-15M ARR | 10-15x EBITDA | PE-backed acquisitions |

| $15-50M ARR | 15-25x EBITDA | Strategic buyers, growth equity |

| $50M+ ARR | 20-35x+ EBITDA | Late-stage PE, pre-IPO |

When to use it: Companies with professional management, positive EBITDA, and revenue above $5M ARR. This is the language PE firms speak, and if your exit will involve private equity, you need to understand EBITDA cold.

Adjusted EBITDA matters more than EBITDA. Buyers will calculate “adjusted” EBITDA, which normalizes for one-time costs, stock-based compensation, and other non-recurring items. The gap between EBITDA and adjusted EBITDA is where deal negotiations live.

Method 4: Discounted Cash Flow (DCF)

DCF is the most theoretically rigorous valuation method. It calculates the present value of all future cash flows the company is expected to generate.

How it works: Project free cash flows for 5-10 years, calculate a terminal value, and discount everything back to present value using a discount rate (usually the weighted average cost of capital, or WACC).

Formula (simplified): Valuation = Sum of (Projected Free Cash Flow in Year N / (1 + Discount Rate)^N) + Terminal Value / (1 + Discount Rate)^N

When to use it: Companies with stable, predictable revenue and clear growth trajectories. DCF is most useful for mature SaaS companies or as a sanity check against multiple-based valuations.

The problems with DCF for SaaS:

- It requires assumptions about future growth rates, margins, and terminal value - all of which are speculative for early-stage companies

- Small changes in the discount rate or terminal growth rate dramatically change the output

- Most SaaS companies do not have enough operating history to build reliable projections

When DCF actually works well:

- Public company analysis

- Large private SaaS companies ($50M+ ARR) with 3+ years of stable metrics

- As a “floor” valuation to complement revenue multiple analysis

- Companies with complex revenue streams (usage-based, hybrid pricing)

The biggest mistake with DCF: Garbage in, garbage out. If your revenue projections assume 50% growth for 10 years with expanding margins, you will get a massive valuation that no one will pay. Use conservative assumptions, and stress-test the model with bear, base, and bull cases.

Method 5: Comparable Transaction Analysis (Comps)

This method values your company based on what similar companies have actually sold for.

How it works: Find recent acquisitions of SaaS companies similar to yours in size, growth, market, and model. Extract the implied multiples from those deals. Apply those multiples to your metrics.

When to use it: Always. Comps should be part of every valuation exercise because they reflect what real buyers actually paid - not theoretical models. The challenge is finding truly comparable transactions, since most private SaaS deals are not publicly disclosed.

Where to find SaaS transaction data:

- SaaS Capital Index (quarterly reports on SaaS multiples)

- SEG SaaS Advisors (publishes transaction data)

- PitchBook and Crunchbase (fundraising rounds)

- Acquire.com marketplace listings (sub-$5M ARR segment)

- Public company filings (10-K, proxy statements for M&A)

The biggest mistake with comps: Cherry-picking the most favorable transactions. A $50M ARR company growing at 80% is not a comparable for your $5M ARR company growing at 20%, even if you are in the same market. Match on size, growth, and stage.

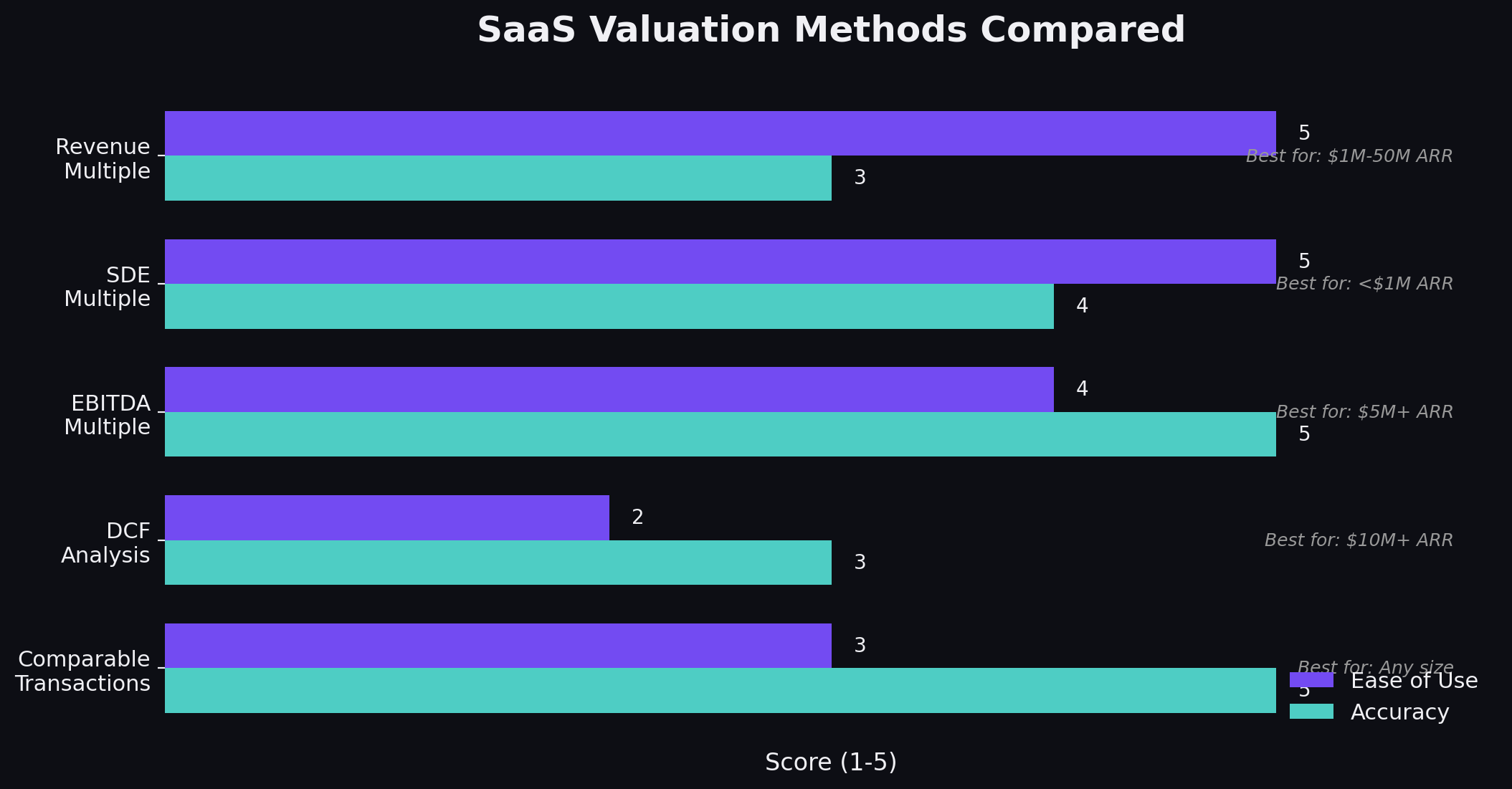

Valuation Method Comparison: Which One Should You Use?

| Method | Best For | Accuracy | Complexity | Buyer Expectation |

|---|---|---|---|---|

| Revenue Multiple | $1-100M ARR, fundraising, M&A | Medium-High | Low | VCs, strategic buyers |

| SDE | Under $5M ARR, bootstrapped, owner-operated | High (for this segment) | Low | Individual buyers, micro-PE |

| EBITDA | $5M+ ARR, profitable, PE exits | High | Medium | PE firms, strategic buyers |

| DCF | $50M+ ARR, stable companies, sanity checks | Varies wildly | High | Institutional investors |

| Comps | All stages (as supplement) | High (if good comps exist) | Medium | Everyone |

Our recommendation: Use revenue multiples as your primary method, comps as your reality check, and DCF only if you have the data to support it. For sub-$5M bootstrapped companies, use SDE. For PE exits, lead with EBITDA.

The Rule of 40: The Single Most Important Benchmark

If you remember one thing from this guide, remember the Rule of 40. It is the closest thing SaaS has to a universal health score, and it is the first thing sophisticated investors look at.

The Rule: Revenue growth rate (%) + EBITDA margin (%) should be greater than or equal to 40%.

Examples:

| Growth Rate | EBITDA Margin | Rule of 40 Score | Assessment |

|---|---|---|---|

| 50% | -10% | 40 | Passing - growth compensates for losses |

| 20% | 25% | 45 | Passing - balanced profile |

| 30% | 15% | 45 | Passing - healthy mix |

| 10% | 15% | 25 | Failing - not growing fast enough to justify low margins |

| 60% | -30% | 30 | Failing - burning too much cash despite growth |

Why it matters for valuations: According to analysis from SaaS Capital (2025 data), companies scoring above 40 on the Rule of 40 trade at a significant premium - often 2-3x higher multiples than companies below the threshold. The Rule of 40 captures the tension between growth and profitability that defines SaaS economics.

The Rule of 40 is not binary. A score of 39 does not mean your company is in trouble. But below 30, you are in value-destruction territory. Above 60, you are in elite company.

What changes the Rule of 40 calculus:

- Early-stage companies (under $10M ARR): Investors expect growth to dominate. A score of 30 with 50% growth and -20% margins is more attractive than a score of 30 with 15% growth and 15% margins.

- Mature companies ($50M+ ARR): Investors expect profitability to contribute. A score of 40 with 10% growth and 30% margins is fine. A score of 40 with 40% growth and 0% margins raises sustainability questions.

The Metrics That Actually Drive SaaS Multiples

Beyond the valuation method you choose, specific metrics move your multiple up or down. Here are the ones that matter most, ranked by impact.

Tier 1: The Big Three

1. Net Revenue Retention (NRR)

NRR measures how much revenue you retain and expand from existing customers, excluding new logos. It is the single strongest predictor of SaaS valuation multiples.

| NRR Range | What It Signals | Multiple Impact |

|---|---|---|

| Below 90% | Leaky bucket - losing revenue faster than expanding | Significant discount |

| 90-100% | Maintaining revenue, not expanding | Neutral |

| 100-110% | Healthy retention with modest expansion | Positive |

| 110-130% | Strong expansion revenue, sticky product | Premium |

| 130%+ | Exceptional - land-and-expand working | Top-tier premium |

Benchmark: The median NRR for public SaaS companies is approximately 110% (Source: KeyBanc Capital Markets, 2025 SaaS Survey). Enterprise SaaS companies average 115-125%. SMB-focused companies average 90-100%.

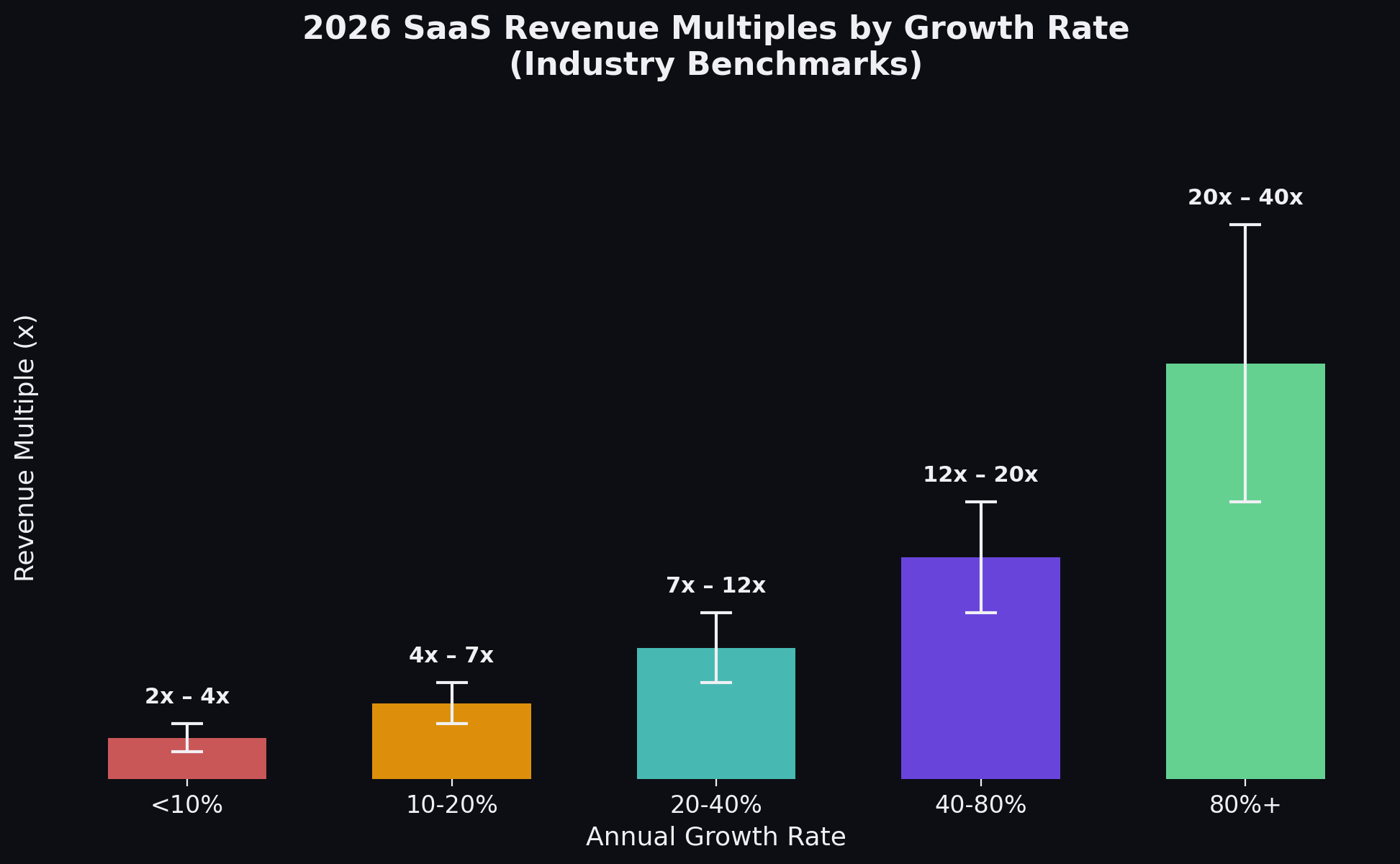

2. Annual Recurring Revenue Growth Rate

Growth is the primary driver of revenue multiples. But the relationship is not linear - growth above 40% commands a disproportionate premium.

| Growth Rate | Impact on Multiple |

|---|---|

| Below 10% | Multiple compression, may trade below 3x |

| 10-20% | Moderate multiples, 3-5x |

| 20-40% | Healthy multiples, 5-8x |

| 40-80% | Premium multiples, 8-15x |

| 80%+ | Top-tier, 15x+, but sustainability questioned |

The growth rate paradox: Very high growth rates (80-100%+ YoY) can actually make sophisticated buyers nervous because they are often unsustainable. A buyer paying 15x ARR is betting that growth continues. If it decelerates sharply post-acquisition, the deal was a bad one.

3. Gross Margin

SaaS gross margins tell you how efficiently the company delivers its product. The margin matters because it defines the ceiling on profitability.

| Gross Margin | Assessment |

|---|---|

| Below 60% | Services business disguised as SaaS |

| 60-70% | Acceptable, but room to improve |

| 70-80% | Healthy SaaS margins |

| 80%+ | Best-in-class |

Tier 2: The Supporting Cast

Customer Concentration. If one customer represents more than 10-15% of ARR, that is a material risk. If the top five customers represent more than 40% of ARR, expect a significant discount. The acquirer is buying revenue, and revenue tied to a single relationship is fragile.

CAC Payback Period. How many months does it take to recoup the cost of acquiring a customer? Under 12 months is excellent. 12-18 months is acceptable. Above 18 months means your unit economics need work before an exit.

LTV:CAC Ratio. The gold standard is 3:1 or higher. Below 3:1 suggests you are spending too much to acquire customers relative to their lifetime value.

Logo Churn. Annual logo churn below 5% is excellent. Between 5-10% is acceptable. Above 10% is a red flag that gets worse with scale.

Burn Multiple. For unprofitable companies: how much cash are you burning per dollar of new ARR? A burn multiple under 1.5 is efficient. Above 2.0, and you are buying growth at an unsustainable rate.

What Doesn’t Work: Common Valuation Mistakes That Kill Deals

After seeing dozens of SaaS transactions from both sides, here are the mistakes that destroy value or blow up deals entirely.

Mistake 1: Conflating revenue with ARR. Professional services, one-time implementation fees, and non-recurring revenue do not get the SaaS multiple. Only true recurring subscription revenue counts. I have seen founders include $500K of professional services revenue in their ARR and wonder why the buyer’s offer was $3M lower than expected.

Mistake 2: Ignoring the quality of revenue. $5M ARR from 500 customers paying $10K/year is more valuable than $5M ARR from 5 customers paying $1M/year. The first has diversified risk. The second has customer concentration that keeps acquirers up at night.

Mistake 3: Using top-of-market multiples from 2021. The SaaS valuation bubble of 2021 produced multiples of 20-40x ARR for growth-stage companies. Those days are gone. According to the SaaS Capital Index, the median SaaS multiple has normalized significantly since then. Using 2021 as your baseline will result in disappointment.

Mistake 4: Neglecting to prepare for due diligence. Buyers will want clean financials, documented processes, a clear cap table, contracts with customers, IP ownership documentation, and employment agreements. Scrambling to produce these during a deal creates delays that kill momentum.

Mistake 5: Waiting until you want to sell to optimize value. Valuation optimization takes 6-12 months minimum. Reducing churn, improving NRR, cleaning up financials, documenting processes - none of this happens overnight. Start preparing at least a year before your target exit date.

Mistake 6: Overvaluing proprietary technology. Your code is not as valuable as you think. Buyers are purchasing cash flows, customers, and market position - not your tech stack. A Rails monolith that generates $10M ARR at 90% margins is worth more than a cutting-edge microservices architecture that generates $2M ARR.

Mistake 7: Founder-dependent operations. If the company cannot operate without the founder for 90 days, the multiple takes a hit. Buyers are acquiring a business, not hiring a new employee. Document everything, delegate decision-making, and build a management layer.

How to Increase Your SaaS Valuation: A Practical Playbook

Valuations are not fixed. They are the result of metrics, positioning, and preparation. Here is what you can do over the next 6-12 months to increase your company’s value.

1. Improve Net Revenue Retention

This has the highest ROI of any valuation optimization activity. Every percentage point of NRR improvement flows directly to your multiple.

Tactics that work:

- Implement usage-based expansion triggers (when a customer hits a usage threshold, present an upgrade path)

- Build an onboarding program that drives time-to-value under 14 days

- Launch a customer success function (even if it is one person) focused on expansion, not just retention

- Introduce annual pricing with built-in escalators (3-5% annual increases)

2. Reduce Customer Concentration

If your top customer is more than 15% of ARR, make it your mission to grow other accounts or acquire new logos that dilute the concentration.

Tactics that work:

- Build a repeatable acquisition channel (SEO, outbound, partnerships) that generates consistent new logos

- Launch an SMB tier with lower price points to diversify the revenue base

- Negotiate multi-year contracts with your largest customers to reduce perceived risk

3. Clean Your Financials

Buyers and investors value clarity. Messy books, combined personal and business expenses, and inconsistent reporting create friction and reduce multiples.

Minimum requirements:

- GAAP-compliant financials (or at minimum, accrual-based accounting)

- Monthly financial packages with MRR, ARR, churn, and NRR

- Clear revenue recognition (especially for annual vs. monthly contracts)

- Documented SDE or EBITDA add-backs with justification

4. Document Everything

Buyers pay a premium for businesses that run without the founder. Documentation is the proof.

What to document:

- Technical architecture and deployment processes

- Customer onboarding workflows

- Sales process and pipeline management

- Hiring, onboarding, and performance management

- Vendor and partner relationships

5. Strengthen Your Market Position

A company that owns its category is worth more than a “me-too” product in a crowded market.

Tactics that work:

- Invest in content marketing and SEO to own category search terms

- Build comparison pages against competitors to control the narrative

- Launch a thought leadership program (newsletter, podcast, speaking)

- Pursue industry awards and analyst recognition

6. Protect Your Intellectual Property

Ensure all IP is properly owned by the company, not by individual founders or contractors.

Checklist:

- All code written by employees or contractors under work-for-hire agreements

- Trademarks registered for company name and product names

- Patents filed where applicable (defensible algorithms, unique processes)

- Domain names, social media handles, and brand assets owned by the company entity

How PipelineRoad Helps with Capital Raising and Valuations

If you are raising capital or preparing for an exit, valuation is only one piece of the puzzle. You also need to identify the right investors or acquirers, build relationships before you need them, and run an efficient process.

PipelineRoad is an AI capital raising platform built for fund managers and SaaS founders. The platform helps you identify the right capital partners, track relationship development, and prepare the materials that sophisticated investors expect. Whether you are raising a Series A or preparing for a PE-led buyout, the fundamentals covered in this guide are what your investors will evaluate.

The 2026 SaaS Valuation Landscape: What Has Changed

The SaaS valuation environment in 2026 is materially different from 2021-2022. Here is what has shifted.

Profitability matters again. The era of “growth at all costs” ended in 2022. Investors and acquirers now want to see a clear path to profitability, even for high-growth companies. The Rule of 40 has gone from “nice to have” to “table stakes.”

AI is a double-edged sword. Companies leveraging AI effectively (in their product, in their operations) can command premiums. But “we use AI” is not a value driver by itself. Buyers want to see AI translating to measurably better margins, faster growth, or stronger retention.

Multiples have normalized but not collapsed. After the 2022-2023 correction, SaaS multiples have stabilized. Good companies with strong fundamentals still command healthy multiples. The companies that were overvalued in 2021 have repriced; the ones with real metrics have held up.

Efficient growth is the new premium metric. Burn multiple (net burn / net new ARR) has become a standard evaluation metric. Investors prefer companies that grow capital-efficiently over those that grow by setting money on fire.

Vertical SaaS commands a premium. Industry-specific SaaS companies with deep domain expertise and high switching costs are trading at premiums versus horizontal SaaS. The specialization creates defensibility that acquirers value.

Building a Valuation Model: Step-by-Step

If you want to model your own company’s valuation, here is the process.

Step 1: Calculate your clean ARR. Strip out non-recurring revenue. Use contracted ARR, not run-rate based on your best month.

Step 2: Determine your primary valuation method. Use the comparison table above to pick the right approach for your stage and situation.

Step 3: Gather your metrics. NRR, gross margin, growth rate, churn, CAC payback, LTV:CAC, customer concentration, burn multiple.

Step 4: Find comparable transactions. Use SaaS Capital, SEG, PitchBook, or public filings to find companies similar in size, growth, and market that have recently transacted.

Step 5: Apply a range, not a point estimate. Any single-number valuation is wrong. Build a bear case (conservative assumptions, bottom-quartile comps), base case (median assumptions), and bull case (optimistic assumptions, top-quartile comps).

Step 6: Adjust for company-specific factors. Apply premiums or discounts for your specific situation: founder dependency, customer concentration, market position, competitive dynamics, IP strength.

Step 7: Reality-test with the market. Talk to advisors, investment bankers, or experienced founders who have been through exits. Theoretical models are useful, but market feedback is what closes deals.

Valuation by Company Stage: What to Expect

| Stage | Typical ARR | Valuation Method | Multiple Range | Key Factors |

|---|---|---|---|---|

| Pre-seed | Pre-revenue | Berkus, Comps | $1-5M post-money | Team, TAM, prototype |

| Seed | $100K-$1M | Revenue multiple (on projected) | $3-10M post-money | PMF signals, early traction |

| Series A | $1-5M | Revenue multiple | 8-15x ARR | Growth rate, retention, unit economics |

| Series B | $5-20M | Revenue multiple, EBITDA | 6-12x ARR | Efficiency, expansion revenue |

| Growth | $20-100M | Revenue multiple, EBITDA, DCF | 5-15x ARR | Rule of 40, market position |

| Pre-IPO | $100M+ | All methods | 8-20x+ ARR | Category leadership, predictability |

| Bootstrapped exit | $1-10M | SDE, Revenue multiple | 3-6x ARR | Cash flow, transferability |

Final Thoughts

SaaS valuations are not mysterious. They are the product of measurable inputs and market conditions. The companies that command premium valuations are the ones that understand their metrics, prepare systematically, and position themselves as category leaders, not just product builders.

If you are thinking about a raise or an exit in the next 12-24 months, start with the Rule of 40. Fix your NRR. Clean your financials. Document your operations. These are not exciting activities, but they are the ones that add millions to your exit price.

The best time to start optimizing your valuation was a year ago. The second-best time is today. If you are preparing investor materials, our SaaS one-pager template guide covers investor, sales, and product one-pagers. And for the market sizing section of your deck, see our TAM SAM SOM guide for SaaS.

Frequently Asked Questions

What is a good valuation multiple for a SaaS company in 2026?

It depends on growth rate, retention, and profitability. The median public SaaS multiple in early 2026 is approximately 6-7x ARR. High-growth companies (40%+ YoY) with strong net retention (120%+) can command 10-15x. Bootstrapped SaaS companies with under $5M ARR typically trade at 3-6x ARR.

How do you value a pre-revenue SaaS company?

Pre-revenue SaaS is typically valued using comparable transaction analysis, the Berkus Method (assigning value to milestones like prototype, team, partnerships), or by estimating future ARR and applying a discounted multiple. Investors also look at TAM, team quality, and product-market fit signals. Be realistic - most pre-revenue SaaS companies raise at $3-8M post-money valuations.

What is the Rule of 40 and why does it matter for SaaS valuations?

The Rule of 40 states that a SaaS company's revenue growth rate plus profit margin should exceed 40%. A company growing at 30% with 15% EBITDA margin scores 45 - healthy. It matters because it balances growth against profitability. Companies above 40 command significantly higher valuation multiples.

Should I use ARR or MRR for SaaS valuations?

Use ARR (Annual Recurring Revenue) for valuations. MRR is useful for internal tracking, but investors and acquirers think in annual terms. ARR = MRR x 12, but only include recurring subscription revenue - strip out one-time fees, professional services, and non-recurring revenue.

When should a SaaS company get a formal valuation?

Get a formal valuation 6-12 months before a planned exit or fundraise. This gives you time to fix issues that suppress value - customer concentration, high churn, missing documentation. Also get one for 409A compliance if issuing stock options, and for estate or tax planning purposes.

Ready to build your SaaS marketing machine?

We have run these plays at 40+ B2B SaaS companies. Let's talk about yours.

Book a Strategy Call